Commentary

The Treachery of Images

Images have always tempted people to produce more of them. Generative AI ushers in the ultimate freedom of the image from human agency.

1.

Gambling is not profane anymore. Consider the mainstreaming of crypto, the retail trading surge of early 2021, and the legalization of sports betting in New York in 2022. Gambling is a subset of speculation, and speculation is at the core of our reality.

Gambling is driven by the desire to maximize time. The more we have to do every day—work, side hustles, endless digital communications, basic life-maintenance—the less time we have. As industry damages the environment, it truncates our capacity as a species to experience time.

Speculation can change time’s shape. It has two main meanings: theorization and investment. The economist Martijn Konings has written on how the popular imagination maintains a distinction between the “fake” value created by speculative investment and the common-sense use value represented by everyday retail purchases. But this distinction is outdated, if it was ever apt in the first place. Like microplastics, speculation has leaked into everything. Financialization is so ingrained that it’s difficult to name a thing that isn’t somehow shaped by speculation.

Like microplastics, speculation has leaked into everything.

When a wager is made, the hallowed outcome always feels like it could happen until it doesn’t. Its contingency gives the passage of time a synthetic thrill. A recent campaign for sports betting company FanDuel by Wieden and Kennedy emphasizes gambling’s temporal aspect. “Make every coin toss feel like a hail mary,” the voiceover says. “Make every moment more heart-racing, zebra-pants wearing, phone-clutching, sitting, standing, solo dancing,” the voiceover says as we see rapid cuts of profitable plays in games and fans celebrating them. Something boring is replaced with something exciting. Without the prosthetics of sports betting, a moment is nothing more than itself.

The FanDuel commercial dramatizes a specific genre of wager called the prop bet. It is not tied to the final score of a game, and it is indifferent to who wins or loses. You can bet on the length of the national anthem, the pregame coin toss result, and the color of Gatorade ritualistically poured on the victorious coach. Through prop bets, bookmakers are able to butcher games into an endless series of over/unders. It’s like being able to turn a single pig into an undepletable source of meat. Every moment is afforded the ability to “mean more.”

2.

The form of the prop bet loosely resembles derivatives trading on the stock market. Popular derivatives include futures contracts, options, and swaps. These contracts derive their value from the behavior of other values: their underlying asset could be a stock or a bond, an index, or another derivative—it could even be the rate of snowfall in a major city during a given time period.

A derivative amounts to a prediction that the value of something will either go up or down. If someone purchases shares of a stock through a spot trade, they can choose to sell it whenever they want, or hold it forever. In their most common forms, derivatives have traditionally had expiration dates that force the trader to wake up from a contractual speculative fantasy. On Wall Street or on Robinhood, the term “future” in “futures contract” refers to a specific date.

Traders can bet large sums of money they don’t have on a prediction of the future that is continually deferred further into the future.

Since 2016, crypto traders have been able to buy and sell perpetual futures contracts. These don’t have an expiration date, and in practice they are often purchased using very high leverage rates, up to 125x. In other words, traders can bet large sums of money they don’t have on a prediction of the future that is continually deferred further into the future. Perpetual futures contracts only expire when a trader elects to close their position, or when they are liquidated, which occurs when they lack sufficient funds to keep a leveraged trade open.

Perpetual futures suggest that we are in a new era of speculative common sense. Sociologist Elena Esposito argued that traditional finance derivatives contracts rewired the internal consistency of linear time by operationalizing the uncertainties of the future to construct prices in the present. Decentralized finance derivatives make things even more complicated by subjecting the triadic relation of past, present, and future to a process of evacuation. Value is able to take leave of earthly temporal limitations. Smart contracts lay claim to immutability through a strange enmeshment of inhuman mechanization. If a wallet is well-funded enough, and a perpetual swap is on-chain, then that swap could ostensibly go on forever. As the expiration of a traditional futures contract edges closer, its price tends to gradually converge with the spot price. In contrast, the price of a perpetual swap never settles because the passage of time cannot be stopped.

3.

Attempts to make time mean more than what it already does mostly fail. Liquidity mining is commonly utilized to make money in crypto, and it’s one of the tools I’ve used the most during my limited experience in the space. In return for giving crypto assets to a decentralized exchange (DEX), a user receives liquidity provider (LP) tokens. Once they have done that, users can elect to stake those LP tokens with a yield aggregating platform and receive potential returns in the form of annual percentage yield, or APY. As one peruses the APYs of various exotic crypto instruments on yield aggregating platforms, measuring possible risks and benefits, the greatest pressure is the need to use time correctly. And yet, tantalizing APYs only generate real value if a series of highly unlikely things happens. Most importantly, highly volatile tokens must not veer toward zero. The best strategy is to be miraculously at the right place at the right time, with plenty of capital already on hand. Most of the time, gambling is not a good way to make money.

If you secure a win while retail trading on the traditional stock market or by betting on sports, it is understood that your gain is somebody else’s loss. Money changes hands, and one starts to wonder about the jackpot’s timeline—what generated these dollars, and what are they taken to measure? The classical labor theory of value postulates that the economic value of a given asset is determined by the labor that produced it. This theory surely doesn’t capture value’s full story within financial capitalism, but it apprehends an important part of it: the question of how value is produced in the first place. It’s deeply challenging to hold onto that thread when considering crypto market dynamics.

Most of the time, gambling is not a good way to make money.

Renegotiating the relationship between time and money through novel blockchain-based financial instruments is arguably a form of gambling. Compared to traditional finance and sports betting, though, the nature of the asset being exchanged, and the question of what creates its value, is even murkier. Where does all that APY come from? Does it measure labor hours? Sort of, probably, I don’t know. Libidinal energy and machines entangle in weird ways to make some horrible void go brr. A governance token I invested in recently lost half its value, in part because holders were disappointed by the results of a new partnership with a DEX: for LP providers depositing a pair of said token and USDC, the DEX only afforded an initial APY of 1200%.

Beefy Finance, a self-described “multichain yield optimizer,” has a recurring piece of copy throughout its interface explaining how its high APYs are achieved. They fill in the blanks with different coins and exchanges for different strategies. “The vault deposits the user’s _____ LP in a _____ farm, earning the platform’s governance token. Earned token is swapped for _____ and _____ in order to acquire more of the same LP token,” it goes. “To complete the compounding cycle, the new _____ LP is added to the farm, ready to go for the next earning event. The transaction cost required to do all this is socialized among the vault’s users.”

There are several other methods of securing promising APYs that I haven’t even touched upon yet, namely ponzinomics, lending platforms, and market-neutral yield farming. Alchemix is one lending platform of particular interest: they offer “self-repaying loans” that claim to completely sidestep the risk of liquidation by supplying borrowers with synthetic versions of the asset they deposit. Hauntingly, one of the slogans on their website is: “Your only debt is time.” Don’t I know it!

4.

Speculation sells the injection of supplementary depth into experience. What’s interesting about this depth, though, is that it reduces complexity rather than enhancing it. When someone refers to a piece of art as “deep” they’re describing it as worthy of contemplation, immersion, and mindful appreciation. None of the characters in the FanDuel commercial want any of those slow, encumbering things. They crave the rush of escape from time. And yet, the only way they know to get this specific rush is mediated by complex speculative instruments.

Instability used to be the last thing anyone wanted. Now it’s a sign of legitimacy, of the real.

Wanting to make the most out of time is an age-old pursuit. Composer Karlheinz Stockhausen approached this question from the angle of sample-based timbre synthesis: “Suppose you take a recording of a Beethoven symphony on tape and speed it up, but in such a way that you do not at the same time transpose the pitch,” he wrote. “And you speed it up until it lasts just one second. Then you get a sound that has a particular color or timbre, a particular shape or dynamic evolution, and an inner life which is what Beethoven has composed, highly compressed in time.” This idea of a symphony compressed into a moment, ready to be sampled and reused as a new sound, feels deeply contemporary.

Speculation often isn’t worth it unless you find a way to rig the game in your favor. How might we make a moment mean less than itself? To me, this sounds much more tantalizing.

The gradual “normalization” of the ongoing financial crisis in recent years has imbued market volatility with a fetishistic charge. Instability used to be the last thing anyone wanted. Now it’s a sign of legitimacy, of the real. If everything is a market, then the applicability of this principle is endless, chopped up into line after line in a back room. Why are so many people swimming in the deep end of risk-tolerance? Have you ever felt a moment that meant more?

Alexander Iadarola is a writer based in New York City. His work has appeared in publications including Rhizome, 032c, and Art in America. He has a blog.

Images have always tempted people to produce more of them. Generative AI ushers in the ultimate freedom of the image from human agency.

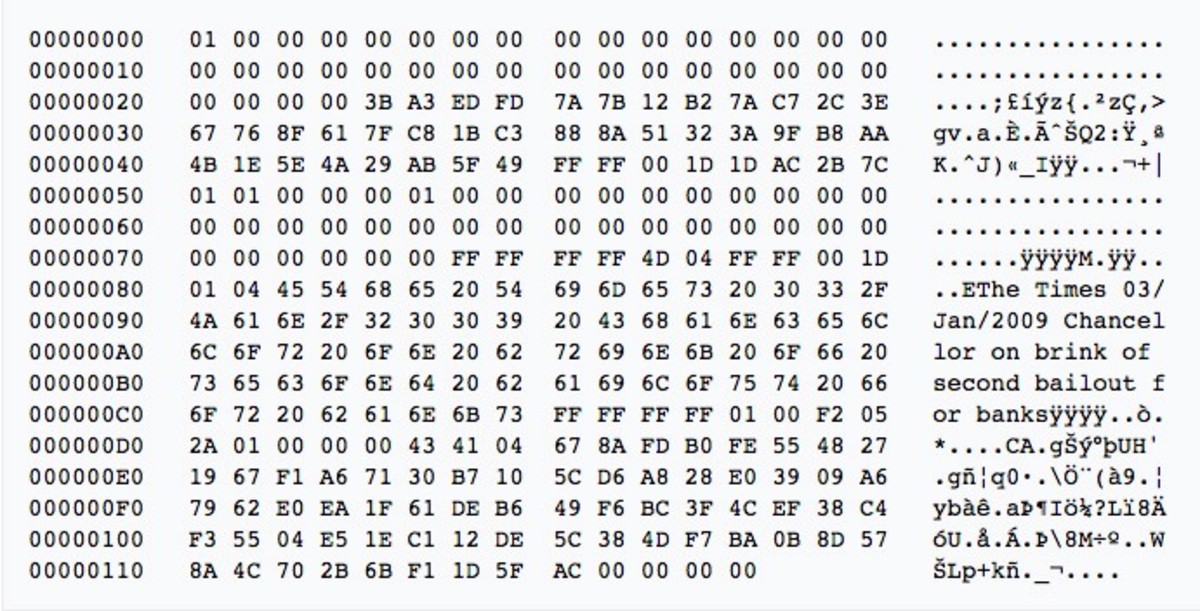

Messages and ASCII art inscribed on the Bitcoin blockchain highlight the human impulse to leave a lasting mark—and to adapt technology for creative purposes.

The investment tools of decentralized finance are accelerating speculation’s spread to all aspects of life, irrevocably changing how we see the world and experience time.